Paying taxes is inevitable, but smart planning can help you reduce the amount you owe and keep more money in your pocket. For W-2 employees, there are three key strategies to explore: maximizing pre-tax contributions, optimizing your withholdings, and starting a business or investing in real estate. Let’s break these down in detail to help you minimize your tax liability.

1. Maximize Pre-Tax Contributions

One of the simplest ways to reduce your taxable income is by contributing to accounts that offer pre-tax benefits. These contributions are deducted from your gross income before taxes, effectively lowering your taxable income. Here are some key accounts to consider:

- 401(k) or 403(b) Retirement Plans

Contributing to your employer-sponsored retirement plan is a powerful way to reduce taxes. In 2025, you can contribute up to $22,500 annually (or $30,000 if you’re age 50 or older). These contributions lower your taxable income while helping you save for the future. - Health Savings Account (HSA)

If you’re enrolled in a high-deductible health plan (HDHP), you can contribute to an HSA. For 2025, individuals can contribute up to $3,850, and families can contribute up to $7,750. HSA contributions are triple tax-advantaged: contributions are tax-free, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. - Flexible Spending Accounts (FSA)

FSAs allow you to set aside up to $3,050 (as of 2025) for qualified healthcare expenses. The money you contribute is pre-tax, reducing your taxable income. Be mindful of the “use it or lose it” rule, as unused funds may not roll over into the next year. - Commuter Benefits

Some employers offer commuter benefits that let you use pre-tax dollars to cover transit and parking expenses, further lowering your taxable income.

By taking full advantage of these accounts, you’re not only saving for essential expenses and future goals but also significantly lowering the amount of income subject to taxation.

2. Optimize Your Withholdings

Another effective way to reduce your tax burden is by ensuring that your withholdings are accurately aligned with your financial situation. Over- or under-withholding can lead to financial inefficiencies, either through large refunds (an interest-free loan to the IRS) or unexpected tax bills. Here’s how to optimize your withholdings:

- Use the IRS Tax Withholding Estimator

The IRS provides an online Tax Withholding Estimator to help you determine the appropriate amount to withhold from your paycheck. By inputting your financial details, the tool will suggest adjustments to your W-4 form. - Adjust Your W-4 Form

Submit an updated W-4 form to your employer if your personal or financial circumstances change, such as:- Getting married or divorced

- Having a child

- Taking on a second job or earning significant non-W-2 income

You can use the withholding estimator results to determine how to fill out the form, such as adjusting the number of dependents, adding extra withholdings, or reducing withholdings if you consistently receive large refunds.

- Plan for Additional Income

If you earn income outside of your W-2 job (e.g., freelance work, investments, or rental properties), consider adjusting your withholdings to account for this additional income. This can help you avoid underpayment penalties.

Optimizing your withholdings ensures you’re paying just the right amount throughout the year, avoiding surprises during tax season.

3. Start a Business and Invest in Real Estate

Starting a business or investing in real estate are powerful strategies for reducing your tax liability while building wealth. Here’s how these approaches can help:

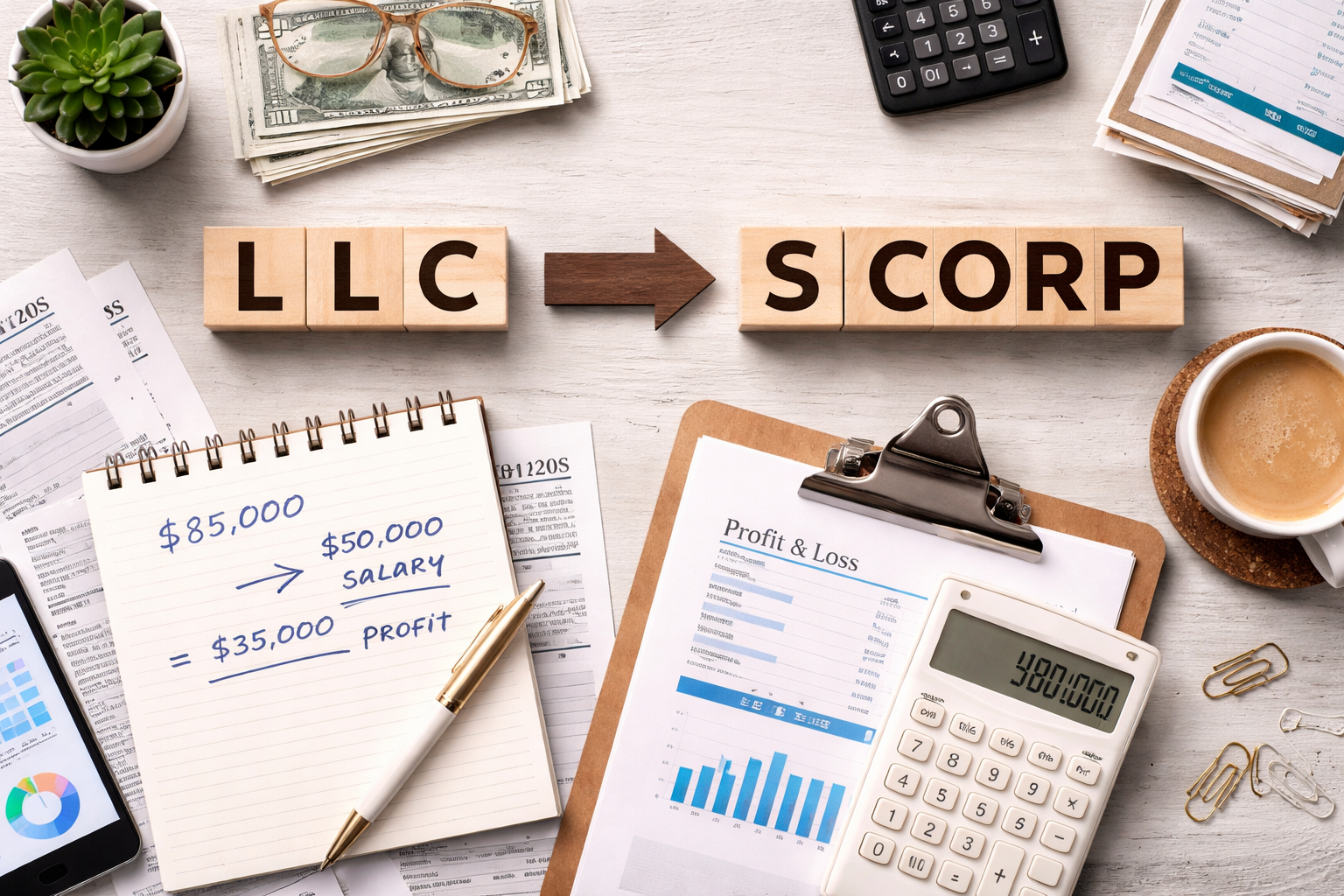

- Starting a Business

As a business owner, you can take advantage of numerous tax deductions that are not available to W-2 employees. These include deductions for home office expenses, vehicle usage, internet and phone bills, and other business-related expenses. Additionally, you can deduct contributions to a retirement plan, such as a SEP IRA or Solo 401(k), which can significantly lower your taxable income. - Investing in Real Estate

Real estate investments offer unique tax benefits, such as depreciation, which allows you to deduct the cost of wear and tear on your property over time. You can also deduct mortgage interest, property taxes, and other operating expenses. If structured properly, real estate investments can generate income while reducing your overall tax burden. - Leverage Tax-Advantaged Strategies

Both business owners and real estate investors can benefit from strategies like pass-through deductions, Section 179 deductions, and cost segregation studies. Consulting with a tax professional can help you identify and implement these strategies to maximize your savings.

Starting a business or investing in real estate not only reduces your taxes but also provides long-term opportunities for financial growth.

Final Thoughts

Reducing W-2 taxes isn’t just about paying less to the IRS—it’s about taking control of your financial situation and making the tax system work for you. By maximizing pre-tax contributions, optimizing your withholdings, and exploring opportunities in business or real estate, you can minimize your tax liability, save for the future, and keep more of your hard-earned money.

If you’re unsure where to start, consult a tax professional who can help you create a personalized strategy. Small adjustments can lead to significant savings over time, so don’t delay in taking action.

No comment yet, add your voice below!